default

The Geothermal Supply Chain Is America’s to Gain — or Lose

A domestic supply chain can de-risk geothermal deployment and spread the economic benefits nationwide.

Introduction

Next-generation geothermal energy shows growing promise as a source of firm, reliable power. Investment in the sector has grown a hundredfold in seven years from $22 million in 2018 to $2.2 billion in 2025; pilot projects are successfully delivering electricity; and the first phase of a large-scale commercial plant, a 500 MW project in Utah, will come online this year.

A growing body of evidence suggests that the geothermal opportunity is particularly large for the United States, which holds the world’s largest technical resource and much of the expertise needed to unlock it. There is growing recognition that, at least in the United States, the sector’s long-term viability depends heavily on progress achieved through the early 2030s, technology transfer from oil and gas, and equipment standardization. These factors make understanding supply-chain readiness, both domestic and global, crucial.

At the rate of deployment needed for national-scale geothermal adoption, equipment supply chains are likely to become a limiting factor. But the United States is well positioned to turn this risk into an opportunity: it possesses the manufacturing expertise needed for geothermal technology adapted from the oil and gas industry and can develop the capacity to manufacture other components. Doing so could spread economic benefits to manufacturing clusters across the country, but the opportunity will not automatically materialize. Capturing the supply chain for next-generation geothermal requires targeted policy and proactive new research.

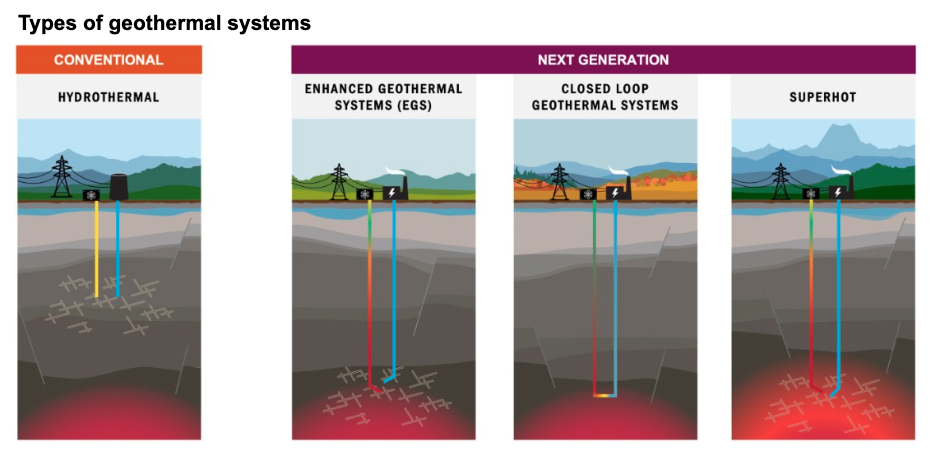

Next-generation geothermal techniques and equipment

Next-generation geothermal refers to approaches that create or control the subsurface conditions needed to extract heat where nature does not already provide a productive hydrothermal system. Enhanced geothermal systems (EGS) create permeability in hot rock; closed-loop systems circulate working fluid through sealed subsurface networks; and superhot rock projects apply these approaches at much higher temperatures and energy densities. These technologies can support direct heat applications as well as electricity generation.

Projects require equipment across four stages: drilling, well construction, heat extraction, and power production. That includes rigs, drill strings, bits, downhole sensing and steering tools, casing, cements, fluid-management systems, pumps, heat exchangers, turbines, condensers, transformers, switchgear, and other grid-connection equipment. The precise mix of equipment varies by technology and firm.

Types of geothermal power systems

The United States has a supply-chain advantage, but gaps remain

Overlaps with oil and gas position the United States as an early leader in the equipment supply chain for next-generation geothermal. The International Energy Agency (IEA) estimates that oil and gas expertise is relevant to more than three-quarters of next-generation geothermal investment. Leveraging this expertise helps reduce project development costs by repurposing capabilities that the oil and gas sector has already spent decades refining. US developers have already drawn on this overlap and are procuring drill rigs, drill bits, well casings, and other key materials from oil and gas service providers.

But as developers target hotter temperatures at greater depths to unlock higher energy density, they will run up against the limits of off-the-shelf oil and gas technology. Standard drill rigs are widely available in North America, but superhot rock (SHR) compatible rigs are much rarer. Conventional drill bits and other components degrade in conditions harsher than those for which they were designed. This has led some developers to draw on supply chains outside of oil and gas for their drilling technology. For example, millimeter-wave (MMW) drilling technology uses gyrotrons, which come from the fusion research industry. Even MMW proponents note that the gyrotron supply chain “currently can’t handle an order for 10 [or] more” units.

Finally, although many surface-plant components are made in the United States, geothermal turbomachinery for power conversion largely is not. The organic Rankine cycle (ORC) turbines used for EGS and the steam turbines proposed for superhot rock are made mostly abroad, though industry stakeholders express optimism about the ability of gas turbine manufacturers in the United States to enter the geothermal market. Some grid-connection equipment, like transformers and switchgear, is available from domestic manufacturers, but long procurement timelines have plagued the energy sector since the pandemic. (For additional detail on component-level supply chains, see Exhibit A2 in the Appendix.)

These dynamics could put the industry in a bind. The uncertain deployment trajectory for next-generation geothermal deters dedicated manufacturing investment, but the absence of a dedicated supply chain raises investor perception of risk and project development costs. Avoiding this bind will require proactive intervention.

Supply-chain buildout offers economic opportunity

Tackling this challenge creates economic opportunities. Building a domestic geothermal supply chain can enable faster deployment, catalyze manufacturing job growth, and drive regional economic diversification.

Building a domestic supply chain enables faster deployment because even at present, equipment supply chains could bottleneck projects. Mitigating that risk can boost investor confidence in the industry. Accelerated project development could eventually create over 100,000 jobs in the development and operation of geothermal wellfields and surface plants. State and local institutions are already partnering with geothermal firms on workforce development.

Investment in geothermal equipment production directly catalyzes manufacturing job growth. The IEA estimates that roughly a quarter of all jobs in conventional geothermal are in equipment manufacturing. If that number is roughly representative of next-generation geothermal, then it is twice the proportion of manufacturing jobs in solar energy. If the United States does not seize the opportunity to capture the jobs in geothermal manufacturing, other countries will.

Different parts of the country can support different parts of the geothermal supply chain. Employment in oil and gas machinery manufacturing, where expertise can transfer to the production of geothermal-compatible drill rigs and mechanical drill bits, concentrates most heavily in parts of Louisiana, Texas, and Oklahoma, as shown in Exhibit 1. Turbine and generator manufacturing employment is heavily located in several eastern states, including parts of Georgia, New York, North Carolina, and South Carolina, as shown in Exhibit 2. Some regions host a high concentration of employment in not just one but several manufacturing activities that relate to the geothermal supply chain, as shown in Exhibit 3. These findings, drawn from RMI’s Clean Growth Tool and displayed below, indicate a wider geography of economic opportunity than maps of geothermal resource potential would imply.

Exhibit 1

Exhibit 2

Exhibit 3

How large this opportunity becomes will depend on how quickly geothermal grows in the United States and abroad and on the competitiveness of American manufacturing. This buildout could take the form of new investment in existing facilities (like gas turbine production plants) or as greenfield project development. Either way, this could benefit regional economies. Many of the industries that overlap with the geothermal supply chain, like oilfield equipment production and turbine manufacturing, have suffered from volatile markets. For regions specialized in these industries, the geothermal supply chain is an opportunity to diversify. If the industry takes off, that new diversification could boost these regions’ economic resilience.

Targeted policy and better data can help grow geothermal manufacturing

Seizing this opportunity will require targeted policy action at the federal and state levels, supported by research that can inform both policy implementation and economic development strategy.

Part of the policy foundation already exists. The 48E electricity investment credit and 45Y electricity production credit, established in 2022 and preserved for geothermal in 2025, provide a decade of runway to project developers in precisely the same years when the industry has the best shot at achieving commercial-scale adoption. These credits matter for supply chain buildout for two reasons. First, repeated infrastructure development gives manufacturers more confidence in the market opportunity. Second, provisions in the credit explicitly encourage domestic manufacturing, but need clarification if they are to achieve their intended effect.

Federal policymakers can also explore strengthening existing programs to provide supply-side support. Expanding the 45X advanced manufacturing production tax credit to the geothermal supply chain, for example, would encourage domestic investment and bridge equipment production cost gaps with overseas suppliers.

States are already moving to accelerate geothermal deployment through policies like Colorado’s geothermal investment credit, and they can do the same for equipment manufacturing. Economic development officials will be vital to the build-out of a dedicated supply chain for geothermal components in the United States because they are responsible for identifying and assessing beneficial economic opportunities in fast-growing markets and ensuring that their community is ready to win investment when the right moment arises.

But for policymakers to effectively implement new programs and for economic development leaders to advance investment attraction strategies for the geothermal supply chain, they need better data. This can include an inventory of equipment and components used in next-generation geothermal projects; estimates of equipment manufacturing capacity, production costs by country, and lead times; and modeling of supply chain buildout scenarios alongside infrastructure development. The Department of Energy (DOE) and national labs are well-positioned to lead research and analysis to build this evidence base, along with other research organizations and institutions that can synthesize insights for policymakers, economic developers, industry, and investors. Research can also examine how both federal and state-level policy can catalyze new investment and jobs in different regions.

Policymakers, economic developers, and industry stakeholders can leverage this data to target the most urgent supply-chain needs first (e.g., through grant allocation or procurement) and ensure that public policy positions American manufacturers for success in this growing global market. For additional detail, see Exhibit A1 in the Appendix.

The window is open today

The long-term trajectory of next-generation geothermal in the United States and worldwide may not become clear for several more years, and equipment supply chains are only one part of this story. But if policymakers neglect the geothermal supply chain, the window of opportunity may be lost.

The United States has forfeited early advantages in energy technology supply chains before. Let’s not do so with geothermal.

RMI works to advance federal and subnational policy and economic development in the United States by highlighting priority research needs in new energy technology supply chains. For more information, please contact the authors at benjamin.feshbach@rmi.org; jmeisel@rmi.org; and egarland@rmi.org.

Appendix

The Exhibits below include a catalogue of equipment and supply-chain information for next-generation geothermal power systems; policy and research priorities for the geothermal supply chain; and RMI’s identification of six-digit NAICS industries that overlap with potential equipment manufacturing needs for next-generation geothermal.[1]

Exhibit A1

Exhibit A2

Exhibit A3

[1] NAICS codes are numerical codes used by businesses and government agencies in Canada, Mexico, and the United States to classify industries based on their primary activity.

Acknowledgments

The authors wish to thank the following individuals for their feedback on early drafts of this piece: Aaron Brickman, Alexander Rutter, Ben King, Jason Lipton, Jake Higdon, Jenna Hill, Hannah Perkins, John Coequyt, Lachlan Carey, Michael Grappone, Nathan Pastorek, Sarah Ladislaw, Terra Rogers, and Wilson Ricks. Inclusion on this list does not indicate endorsement of the findings in this piece.

The New Energy Industrial Strategy Center

The NEIS Center is a thought partner, funder, and community builder that helps create advanced energy systems that support competitive economies and power the industries of the future.